Committee on Women’s Rights and Gender Equality (FEMM)

With some European countries applying up to more than 20 percent tax on feminine hygiene products, classifying them as non-essential goods, what steps should the EU take to further fight the pink tax and period poverty?

Chairperson: Pol Sanmartí (ES)

INTRODUCTION

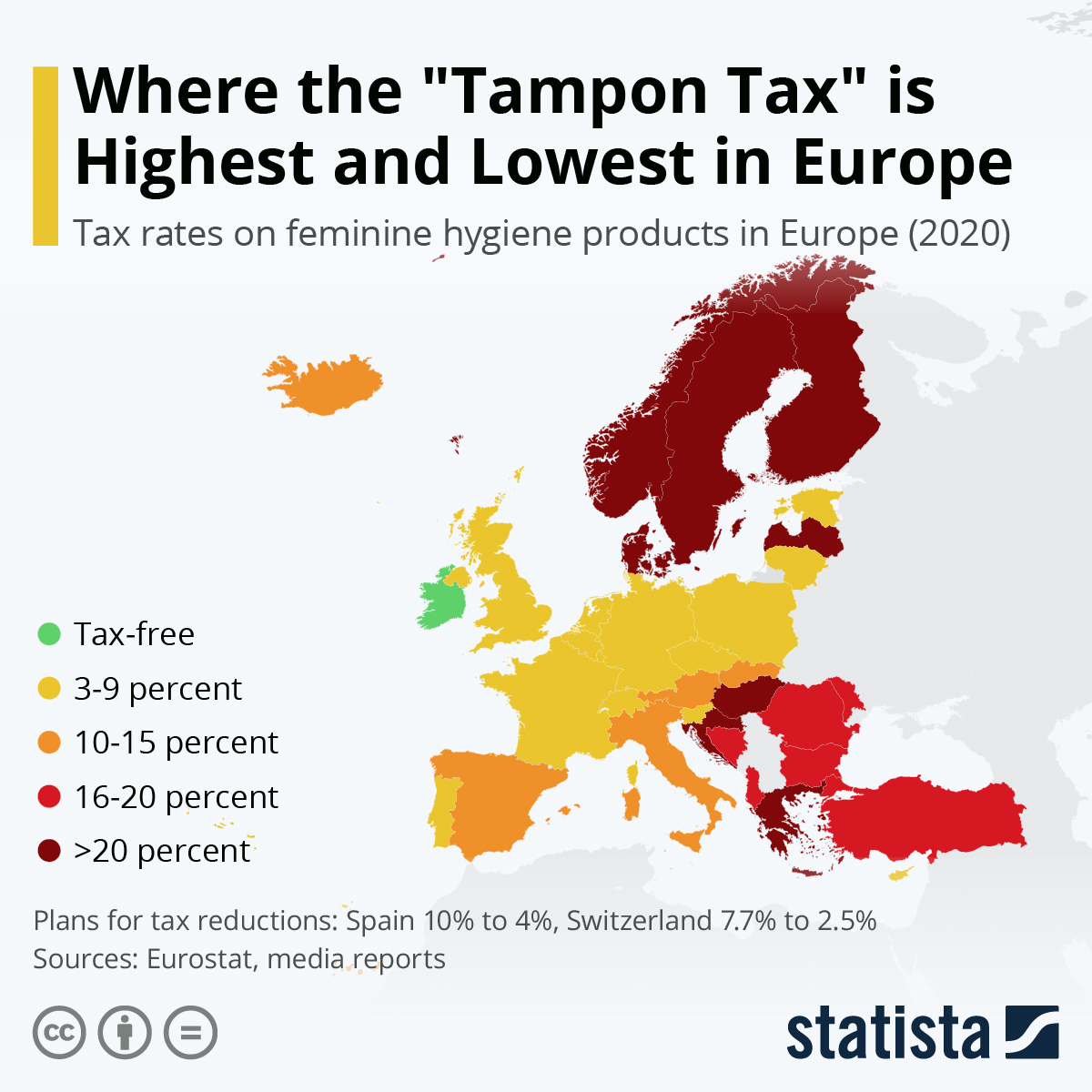

With the rise in the feminist wave throughout Europe, the Pink Tax still poses an obstacle to obtaining gender equality. In the EU, although countries can apply super-reduced tax rates to feminine sanitary products since 2007, countries like Hungary (27% tax), the Scandinavian Region (25% tax), or Greece (23% tax) maintain higher taxes on them, according to Eurostat. Some countries such as Greece justify this as austerity measures1Austerity measures are economic policies implemented by governments to reduce public debt and to shrink the budget deficit.. Regardless, seeing how 1 in 10 girls can not afford sanitary products in Europe, the “tampon tax” raises a question on financial and social equality.

Some EU countries have started tackling the problem with the reduction of Value Added Tax (VAT)2VAT is a consumption tax added to every product at every point of the supply process where value is added to it. It is therefore paid for by the consumer, adding to a product’s original production price. on feminine hygiene products. France (5.5% tax) and The Netherlands (6% tax) are such examples. But seeing how VAT legislation is in Member States governments’ competencies, within some limits set by the EU, equity throughout Europe can not be ensured. As long as EU countries treat period products as luxury goods, there will be no room for change. The question raised is thus of both economic and social importance: on the one hand, there is a higher burden on women for their hygiene products. On the other hand, a breach in Article 23 or the Charter of Fundamental Rights of the European Union (CFR), can be argumented, raising ethical implications of gender-based discrimination.

KEY TERMS

- Luxury versus essential goods: Luxury goods are not necessary to live, but deemed highly desirable. On the other hand, essential goods are crucial for day-to-day life. EU VAT policy distinguishes between rates for both types of goods.

- Pink Tax: The tax is a gender-based price discrimination3Price discrimination happens when a seller charges customers a different fee for the same product or service. practice that causes women to pay higher prices than men for identical or substantially similar goods and services. It also happens with period hygiene products as they are considered luxury instead of essential goods by many countries.

- Gender equality: as defined under Title III of the Charter of Fundamental Rights of the EU, all men and women shall be equal in all areas, which includes VAT taxing on goods.

- Reduced, super-reduced, and zero rates: Reduced rates are applied to goods specified under Annex III (referring to Article 98) of the VAT Directive, which allows up to two reduced VAT rates of 5%. Moreover, super-reduced rates and zero rates allow for exceptionally reduced rates on sales for EU members. Some EU countries use these on period products.

MAIN ACTORS

- European Institute for Gender Equality (EIGE): is a European agency that works to promote and ensure equal opportunities for women and men across Europe through quality evidence for better policy making. It works on four main areas: gender mainstreaming, gender-based violence, gender statistics, and the Beijing Platform of Action (the emphasis shall be put on the two latter for this committee).

- The European Commission is the executive branch of the EU, in charge of proposing legislation, implementing decisions and managing the day-to-day business of the EU. By promoting initiatives on gender equality in collaboration with the EIGE or the CSW, the European Commission seeks to tackle gender-related issues. They are currently abiding by a 5-year plan called the Gender Equality Strategy 2020-2025.

- Commission on the Status of Women (CSW) is a functional commission of the UN Economic and Social Council (ECOSOC) is the main global intergovernmental body exclusively dedicated to the promotion of gender equality. In collaboration with the EU and based on the Beijing Platform for Action, they work on the implementation of Goal 5 of the UN Sustainable Development Goals (SDGs) in the EU.

MEASURES IN PLACE

The EU Gender Equality Strategy is the main EU-driven project concerning gender equality issues. Although it takes gender issues as a whole, abiding by the Gender Equality Strategy 2020-2025, it includes all issues regarding equality. As stated in the CFR, the right to gender equality is a key pillar of the EU. However, no specific committees or legislation has been drafted on the topic of the ‘pink tax’ at EU level.

Another EU initiative is the Gender Action Plan II (GAP II). Their role is to oversee that all development programmes, projects and action documents deliver more effectively on the commitments towards gender equality and women’s and girls’ empowerment. Although it ensures EU’s willingness to further gender equality internationally, the framework is broadly defined and does not offer concrete deadlines and objectives.

The Beijing Platform for Action is relevant as an international conference on women rights of the UN, held in 1995. The Beijing Declaration and Platform for Action resulted from the conference, providing a guideline for change in terms of gender equality around the world. The importance of this document is in how it serves as a starting point for EU dealings on the topic, seeing how the EIGE is partly dedicated to it.Finally, concrete VAT measures are taken by national and regional governments, as specified throughout this document. France and Ireland would be examples of countries that apply reduced and 0% VAT rates respectively. But with the current situation, no EU-wide action has been taken on the issue, leading to very heterogeneous taxing strategies and creating inequalities between women in different EU States.

KEY CONFLICTS

“I think the motivations around the pink tax come more explicitly from a classic capitalist stance: If you can make money off of it, you should,” explains Jennifer Weiss-Wolf, Vice-President of the Brennan School of Justice at NYU School of Law. It is clear that being in a union of capitalist countries, although to different degrees, it can be argued that a tax on feminine hygiene products is appealing for governments, knowing that the demand elasticity4Low demand elasticity refers to the situation when demand for a good is not greatly influenced by a change in the price of said good. will be low. Consequently, they are viewed as a reliable source of income for governments. Nonetheless, seeing how the EU has introduced low VAT rates for goods deemed necessities, would it not be ethical to consider hygiene products, such as period products especially, as essential necessities for women and consequently apply reduced taxes? It becomes a question of whether a free market economy should prevail, or whether human rights and equality should do so?

With the EU having limited restrictions and rules on VAT taxing, and currently having no competence on Member States taxing, an issue appears. The Pink Tax burdens all EU States, but whether this burden is or not tackled, depends on local governments’ projects and views. Consequently, some countries perpetuate gender inequality by allowing the tampon tax and fostering period poverty. This also perpetuates cross-national inequality, as different countries tax differently, or do not tax at all, on feminine hygiene products. But should the EU transgress into national competences for the particular case of the tampon tax? Is this case of gender inequality enough to justify a possible change in EU competences in national economic policies?

FOOD FOR THOUGHT

Seeing how some EU citizens are still subject to unequal taxing on products targeted to their specific gender, having to spend more money than their male counterparts, this is an issue of both economic and social nature that concerns human rights. Both ends of the spectrum should be considered: both the profit-based capitalist vision and the gender-equality-oriented stance. Moreover, seeing how taxing policies differ between regimes and governments, and how little power the EU holds on policy proposals regarding those topics, an innovative approach has to be taken if a solution has to be found.

- Can the Pink Tax be attributed to free-market capitalist mechanisms? And if so, does this justify its existence?

- To what extent are high VAT rates for feminine hygiene products linked to gender discrimination?

- Should there be EU-level legislation concerning the taxing of feminine hygiene products specifically?

LINKS FOR FURTHER RESEARCH

- Why you should keep paying the ‘tampon tax’ (2018) article by Jessica Irvine on some benefits of having a tampon tax.

- VAT rules and rates: standard, special & reduced rates – official website with explanations about European VAT rules and rates.

- Periods aren’t a luxury. Why are they taxed like one? (2018) TED Talk by Linda B. Rosenthal on why the tampon tax should be eradicated.

- Period Poverty : Breaking The Silence (2017) – TEDx Talk by Amika George on period poverty and its repercussions.

- Does Ireland Have A Tampon Tax? We Investigate (2020) article by Kate Demolder for the Irish Tatlet on what is the tampon tax and why do people pay it in Ireland.

- Gender Equality Strategy 2020-2025

- VAT Directive